Running a business involves more than generating revenue. Understanding the different Types of Expenses in Accounting is essential for accurate financial reporting, compliance, and effective cost management. Classifying and monitoring these expenses helps business owners maintain financial transparency and make informed decisions.

This article explains the main expense categories in accounting, their importance in financial management, and how they influence financial statements.

What Are Expenses in Accounting?

Expenses represent the costs a company incurs to operate and generate income. Common examples include rent, salaries, utilities, marketing, and travel. These are listed on the income statement and directly affect a business’s profit or loss.

By analyzing expenses, businesses can identify where money is being spent, assess profitability, and maintain accurate financial statements that meet regulatory and investor requirements.

Why Expense Classification Matters

Accurately classifying expenses offers several benefits:

- Better cost forecasting and budgeting

- Compliance with accounting and tax regulations

- Clearer financial reporting for audits and investors

- More efficient operational and investment planning

Many businesses in the UAE partner with professional accounting services to ensure expense reporting is accurate, compliant, and aligned with local financial standards.

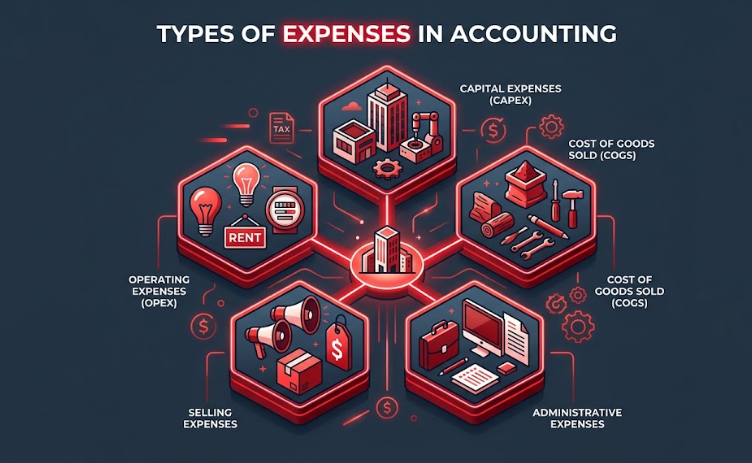

Main Types of Expenses in Accounting

Below are the principal categories every business should understand when managing its accounting records.

1. Capital Expenses (CAPEX)

Capital expenses are investments in long-term assets that benefit the business over several years. These costs are capitalized and depreciated over time rather than recorded as immediate expenses.

Examples:

- Office buildings and improvements

- Machinery and equipment

- Company vehicles

- Technology infrastructure

Correctly identifying and recording CAPEX is critical for long-term financial planning and compliance with accounting standards.

2. Operating Expenses (OPEX)

Operating expenses include the day-to-day costs required to keep a business running. While they do not directly produce goods or services, they are necessary for continued operations.

Examples:

- Rent and utilities

- Office supplies and services

- Marketing and advertising

- Insurance and administrative costs

Properly managing operating expenses allows companies to maintain efficiency and control recurring costs.

3. Tax Expenses

Tax expenses refer to obligations such as VAT, corporate income tax, and other government levies. Estimating and recording these accurately ensures full compliance and helps avoid penalties or misstatements in financial reports.

4. Depreciation and Amortization

Depreciation applies to tangible assets like equipment, while amortization relates to intangible assets such as patents or software. These non-cash expenses spread the cost of assets over their useful life, providing a realistic view of value and profitability.

Accurate depreciation and amortization records are vital for financial statements and when seeking investment or financing.

5. Cost of Goods Sold (COGS)

COGS represents the direct costs associated with producing goods or delivering services. It directly impacts a company’s gross profit margin and overall profitability.

Includes:

- Raw materials

- Direct labour

- Production or service-related costs

COGS is especially important for manufacturing, trading, and retail businesses when assessing operational performance.

6. Non-Operating Expenses

Non-operating expenses are irregular or one-time costs that occur outside normal business activities.

Examples:

- Losses from asset sales

- Legal settlements

- Foreign exchange losses

While infrequent, these costs can affect overall profit and must be disclosed accurately in financial reports.

7. Financial Expenses

Financial expenses include the costs of financing and managing financial transactions.

Examples:

- Interest on loans

- Bank service charges

- Currency conversion costs

Monitoring these expenses helps control borrowing costs and preserve profitability.

8. Selling Expenses

Selling expenses are directly related to promoting and distributing a company’s products or services.

Examples:

- Sales commissions

- Advertising costs

- Shipping and logistics

- Event and trade show expenses

Tracking these expenses enables businesses to evaluate the return on marketing and sales efforts.

9. Administrative Expenses

Administrative expenses cover the general costs of running an organization that are not directly tied to production or sales.

Examples:

- Salaries of management and support staff

- Office rent for administrative departments

- Professional services such as accounting and legal fees

Regularly reviewing these expenses helps businesses identify opportunities for cost optimization and improved efficiency.

How Expenses Appear in Financial Statements

Each type of expense plays a role across the main financial statements:

- Income Statement: Lists all operating and non-operating expenses to determine net profit or loss.

- Balance Sheet: Reflects accumulated costs and investments as assets or liabilities.

- Cash Flow Statement: Tracks how expenses impact operating, investing, and financing cash movements.

Accurate classification ensures a realistic picture of a company’s financial health.

Best Practices for Expense Management

To maintain accuracy and efficiency, businesses should:

- Use reliable, cloud-based accounting software for continuous tracking

- Establish internal approval and documentation controls

- Reconcile expenses monthly to avoid discrepancies

- Engage trusted accounting firms in the UAE for professional oversight

These steps support financial transparency and long-term cost control.

The Role of Accounting in Expense Management

Accounting provides the foundation for effective expense control. Understanding different types of expenses in accounting allows decision-makers to:

- Plan strategically and allocate resources efficiently

- Eliminate unnecessary spending

- Ensure tax compliance

- Build confidence with investors and stakeholders

Accurate accounting contributes to business stability, compliance, and growth.

Conclusion

Every business, regardless of size or sector, should understand the different types of expenses in accounting and their effect on financial performance. Proper classification helps ensure compliance, accurate reporting and stronger cost control.

Analyzing expense categories provides a clear view of where funds are allocated and supports better decision-making, whether accounting is managed internally or outsourced.

How We Helps?

We provides comprehensive accounting services in the UAE, designed to simplify financial management and improve reporting accuracy. By combining technology-driven platforms with professional accounting support, we help your organization stay compliant, gain real-time insights, and focus on strategic growth.

Get in touch with us today to enhance cost control, strengthen financial transparency, and optimize accounting performance across all types of business expenses.